Impact of pandemic on prospects for foreign direct investment

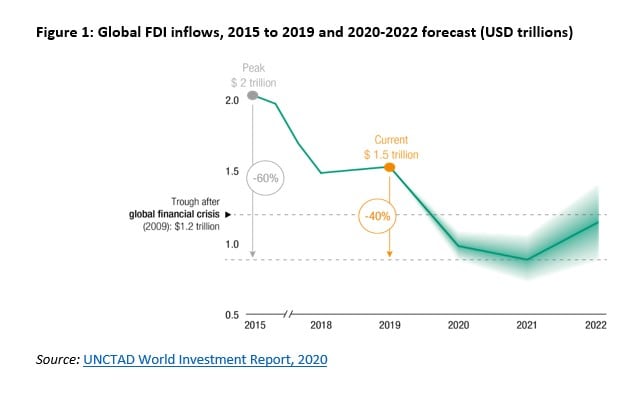

The COVID-19 crisis will cause a dramatic fall in foreign direct investment (FDI). According to UNCTAD’s World Investment Report 2020, global FDI flows are forecast to decrease by up to 40 per cent in 2020, from their 2019 value of $1.54 trillion (figure 1). This would bring FDI below $1 trillion for the first time since 2005.

FDI is projected to decrease by a further 5 to 10 per cent in 2021 and to initiate a graduate recovery in 2022. A rebound, with FDI reverting to the pre-COVID underlying trend in 2022, is possible, but only at the upper bound of expectations. It would show a U-shape recovery. This is unlike the forecasts for global GDP and trade, which are projected to have a V-shape recovery next year.

This outlook is highly uncertain. It will depend on the duration of the global crisis and on the effectiveness of policy interventions to mitigate the economic effects of the pandemic. Geopolitical and financial risks and continuing trade tensions add to the uncertainty.

The projected fall is significantly worse than the one experienced in the years following the global financial crisis. At their lowest level ($1.2 trillion) then, in 2009, global FDI flows were some $300 billion higher than the bottom of the 2020 forecast.

The downturn caused by COVID-19 follows several years of negative or stagnant FDI growth; as such it compounds a longer-term declining trend. The expected level of global FDI flows in 2021 would represent a 60 per cent decline since 2015, from $2 trillion to less than $900 billion.

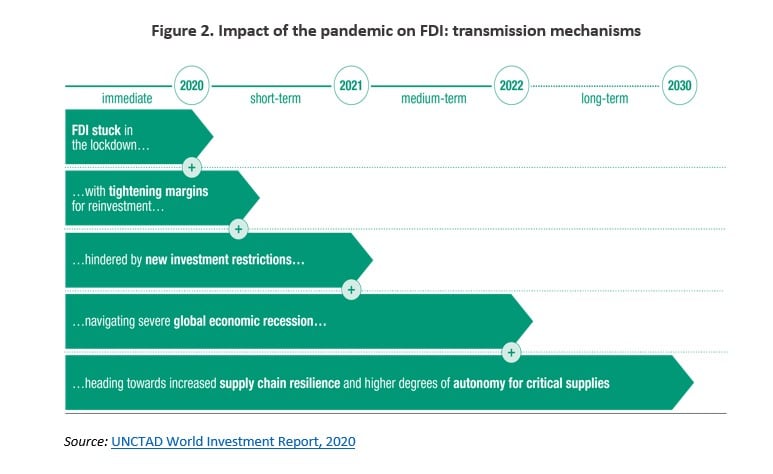

The pandemic is a supply, demand, and policy shock for FDI. It has short-, medium-, and long-term effects (figure 2). The lockdown measures are slowing down existing investment projects. The prospect of a deep global recession will lead multinational enterprises (MNEs) to re-assess new projects. Policy measures taken during the crisis include new investment restrictions. Longer term, investment flows will slowly recover starting 2022, led by global value chain (GVC) restructuring for resilience, replenishment of capital stock and recovery of the global economy.

Over the two critical years of 2020 and 2021, the demand shock will be the biggest factor pushing down FDI. Although in general the trend in FDI reacts to changes in GDP growth with a delay, the exceptional combination of the lockdown measures and the demand shock will cause a much faster feedback loop on investment decisions. The demand contraction hit FDI in the first half of 2020 and then fully unfold in the second half and 2021.

Early indicators confirm the immediacy of the impact. Both new greenfield investment project announcements and cross-border mergers and acquisitions dropped by more than 50 per cent in the first months of 2020. In global project finance, the number of new deals fell by more than 40 per cent.

MNE profit alerts are an early warning sign. The top 5,000 MNEs worldwide, which account for most of global FDI, have seen expected earnings for the year revised down by 40 per cent on average, with many industries plunging into losses. Lower profits will hurt reinvested earnings, which account for more than 50 per cent of FDI on average.

In terms of the severity of the earnings revisions, services industries directly affected by the lockdown are among the most severely hit, particularly travel and leisure sectors. Commodity-related industries suffer from the combined effect of the pandemic and plummeting oil prices. In manufacturing, some industries that are GVC-intensive, such as automotive and textiles, were hit hard by supply chain disruptions. Because of their cyclical nature and global spread, they are vulnerable to both supply and demand shocks. Overall, industries that are projected to lose 30 per cent or more of earnings together account for almost 70 per cent of FDI projects.

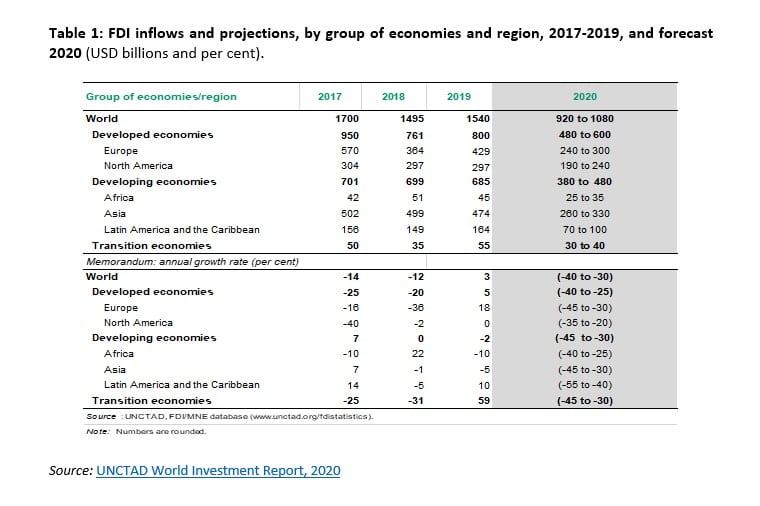

The impact is severe everywhere but varies by region. FDI flows to developing economies are projected to decrease by 30-45 per cent, while 25-40 per cent to developed economies. Developing economies are expected to see the biggest fall in FDI because they rely more on investment in GVC-intensive and extractive industries and because they are not able to put in place the same economic support measures as developed economies. (Table 1)

Despite the drastic decline in global FDI flows during the crisis, the international production system will continue to play an important role in economic growth and development. Global FDI flows will remain positive and continue to add to the existing FDI stock, which stood at $37 trillion at the end of 2019.