Sustainable Finance in European Mid-Cap Markets – Regulatory Complexity, SME Reporting and Green Lending Solutions

With over 2,400 ESG regulations worldwide1, sustainability reporting has become a key part of a company’s entity-level and product-level compliance. In the past decade alone, analysis by ESG Book (2023) found that ESG regulations have increased by 155 percent globally, with 1,255 ESG regulations introduced since 20112.

Regardless of the complexity, sustainability regulations are designed to help companies, investors and banks allocate investment and capital decisions according to their sustainability preferences, and towards sustainable outcomes. Meanwhile, sustainability-related disclosure regulations around the world have been focused on mitigating greenwashing risks to ensure an improved data and information flow and thus drive better decision-making, against the hierarchy of marketing labels.

The European Union, in particular, has been at the forefront of the ESG regulatory movement, introducing comprehensive policies and frameworks that have far-reaching implications for businesses, investors and service providers operating within its jurisdiction.

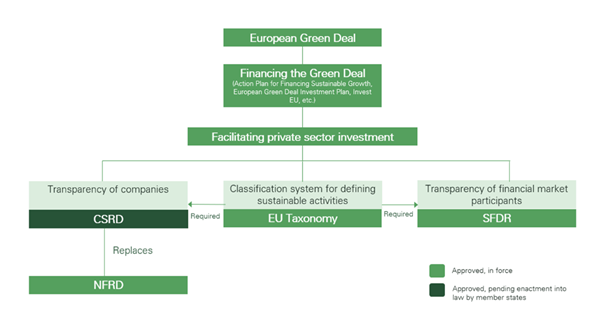

The introduction of the European Green Deal (2019) marked the starting point of a series of pivotal EU disclosure and reporting regulations that are reshaping the corporate, investment, banking and provider landscape. Key regulations linked to the EU’s Green Deal and to the EU’s Sustainable Finance Action Plan3 include:

-

the EU’s Sustainable Finance Disclosure Regulation (EU SFDR) which mandates sustainability reporting for investment managers in the EU, aiming to increase transparency in how financial market participants integrate ESG risks into their investment decisions;

-

the EU’s Corporate Sustainability Reporting Directive (EU CSRD) which expands sustainability reporting requirements for EU and non-EU companies, enhancing the consistency and comparability of sustainability information;

-

the EU’s ‘Fit for 55’ Package - a comprehensive plan to reduce EU greenhouse gas (GHG) emissions by at least 55 percent by 2030, incorporating various legislative measures to support this goal;

-

the EU Taxonomy (EUT) which establishes a classification system for environmentally sustainable economic activities, guiding investment towards more sustainable projects;

-

the EU’s "Fund Names Regime" for sustainable investment products which updates the EU’s Ecodesign Directive to impose stricter requirements on product design for improved environmental sustainability and circularity.

EU ESG Regulatory Overview

Source: Onetrust, Guide to European Regulation, 2024

In addition, a range of new EU regulatory initiatives such as the EU Corporate Sustainability Supply Chain Directive (EU CSDDD)4, help ensure that companies not only report their impacts but also actively engage in accountable sustainable practices to meet the EU's goals of environmental protection, human rights and sustainability in global supply chains.

Given that ESG metrics enforced by the plethora of global sustainability standards and regulations, and additionally a broad range of normative, accounting-linked reporting efforts such as the IFRS’ International Sustainability Standards Board (ISSB), the Task Force on Climate-Related Disclosures (TCFD), the Taskforce on Nature-Related Disclosures (TNFD), the Sustainable Finance Disclosure Regulation (EU SFDR), the UK’s Climate Reporting and the EU’s Corporate Sustainability Reporting Directive (EU CSRD) make it clear to market participants that ESG is no longer optional if they want to remain commercially viable – at entity and at product level.

Simultaneously, governmental regulations may encompass more than reporting obligations, restrictions and environmental requirements. They can also include incentives such as subsidies, grants for green practices and tax measures aimed at promoting sustainable initiatives. Although the regulatory frameworks issued by the European Union are uniformly applicable across its member states, individual countries retain the autonomy to enact national legislation and implement distinct practices that foster sustainable business. Moreover, the private sector enjoys considerable flexibility to develop its own programs and frameworks aimed at encouraging the adoption of ESG principles.

A growing body of academic research and industry studies that highlight the close relationship between sustainability performance and financial results, for example, cost to capital or share-price ratios, has ensured that sustainability issues are being taken into account alongside geopolitical and macroeconomic challenges.

That said, many companies are still transitioning toward ESG becoming truly embedded in their day-to-day business, investment decisions and capital markets allocations, that is, in their banking and lending processes. Addressing regulatory complexity is paramount, at entity and at product level. Small to medium-sized companies (SMEs) face a particular challenge and burden when and where sustainability expertise, operations, monitoring and reporting are concerned.

The European Commission estimates that the EU’s CSRD will eventually impact c.50,000 companies, of all sizes. SMEs account for 90 percent of businesses globally and for 99 percent of the EU’s economy5, and their active participation in ESG disclosure and reporting has the potential to have a significant impact on the transition towards a sustainable and net-zero economy.

Banks providing access to mid-cap-financing and lending aim to ensure that they capture the sustainability profile and activities of their SME corporate borrowers, i.e. their clients, that seek funding in line with green performance criteria and metrics and transition finance requirements. Meanwhile, they also seek downside protection from potential greenwashing risks, default and stranded assets.

Normative and regulatory sustainability disclosure and green lending assessment frameworks can enable banks to identify the most responsible businesses on their books and balance sheets, and support them with climate and sustainability-linked risk stress test scenarios and regulatory reporting requirements, e.g. in line with EU’s Banking Book Taxonomy Alignment Ratio (EU BTAR).

However, SMEs and banks reporting on ESG and climate risk and transition management trajectories nowadays commonly face multiple challenges linked to an ever-increasing number of new frameworks and regulatory reporting requirements, manual, operational workflow processes and thereby rising infrastructure, operational risks and resource costs. Increasingly, they are looking to externalise and automate their ESG operations.

At SIX Financial Information, we have been working with leading industry and policy experts and our co-creation partner, Greenomy, to establish the SIX SME Sustainability Assessment Solution, powered by Greenomy6.

The SIX-Greenomy partnership, announced at COP 28 in Dubai last year, provides tangible benefits for SIX’ and Greenomy’s clients: it reduces the manual reporting burdens, minimises greenwashing risks and enables an easy integration of regulatory parameters and requirements. This addresses the real-world ESG reporting challenges, especially for mid-sized banks and SME companies.

The software-as-a-service (SaaS) is an end-to-end data management and workflow solution that enables SIX’ global banking clients to measure the sustainability performance of their SME clients in a standardised way. The solution maps ESG criteria embedded within multiple regulatory EU frameworks, with the aim to guide corporates and banks through the multiple layers of reporting requirements.

The SaaS solution may evolve in line with market practice and may also be expanded towards common voluntary frameworks, such as the ISSB guidelines and the Global Reporting Initiative’s (GRI) frameworks. Further global frameworks for reporting and disclosure are in scope, providing the basis for additional features and functionalities related to regulatory data, metrics, mapping, benchmarking and screening - and addressing the next challenge: framework interoperability.

To note: This article is a synopsis summary of a chapter on regulatory developments in sustainable finance, published by Lucerne School of Business (Institute of Financial Services) in its “IFZ Sustainable Lending Monitor”. The 2024 study and report will be supported and sponsored by SIX Financial Information. The authors would also like to thank François-Guillaume de Lichtervelde at Greenomy for his key contributions and inputs.

Footnotes

1 For further information, see Plan A Academy, ESG Regulatory Summary, 2024, https://plana.earth/academy/eu-esg-regulations

2 Source: ESGBook, ESG Regulation increases by 155 % over the Past Decade, in ESG News, 20 June 2023, https://esgnews.com/global-esg-regulation-increases-by-155-over-the-past-decade/

3 For further references, please see EU Commission, Sustainable Finance Overview, https://finance.ec.europa.eu/sustainable-finance/overview-sustainable-finance_en

4 For further references, see Onetrust, Ultimate guide to the EU CSRD ESG regulation for businesses, Blog, 2024, https://www.onetrust.com/blog/ultimate-guide-to-eu-csrd-esg-regulation-for-businesses/

5 World Economic Forum, These Charts Show which Businesses are Driving the EU Economy, Blog, 9 January 2024, https://www.weforum.org/stories/2024/01/chart-drive-eu-economy-small-business-sme/#:~:text=Globally%2C%20SMEs%20make%20up%20about,for%20over%20100%20million%20jobs

6 For further information, please visit SIX’ website: https://www.six-group.com/en/products-services/financial-information/esg-data/esg-solutions.html#:~:text=The%20SIX%20SME%20Sustainability%20Assessment,their%20climate%20and%20sustainability%20risk

Disclaimer:

The views, thoughts and opinions contained in this Focus article belong solely to the author and do not necessarily reflect the WFE’s policy position on the issue, or the WFE’s views or opinions.