Green Equity Momentum

Green equity is showing a promising beginning, building on the strengths of the green-bond market. While it took several years from the beginning of the green-bond market to establish guiding market principles and eventually expand to emerging markets, consensus and regional diversification are happening at a faster pace with green equity.

It took several years from the first labelled green bond issued by the World Bank in 2008 until the market saw broad alignment across stakeholders on guiding principles with the International Capital Market Association (ICMA) Green Bond Principles in 2014. While the green bond market was largely a European and multi-lateral institution market in the beginning, by 2016 issuance in emerging markets and especially in China had started to take off.

In contrast, it took only two years from when the first labelled green equity company listed on an exchange, when Nasdaq launched its green equity designations in 2021, to broad alignment across stakeholders on guiding principles with the World Federation of Exchanges (WFE) Green Equity Principles published in 2023. By 2024 there was significant movement in emerging markets with B3 launching a green equity designation in Brazil and the Philippines publishing a draft green equity framework for comment.

While we are only at the beginning of the story for green equity, this early momentum looks favourable for future growth.

How Green Equity Works

Green equity refers to listed companies that demonstrate a contribution to the green economy, according to the specific requirements of different stock exchanges. The green label is typically conferred based on an independent external review that the company meets the requirements of the exchange, similar to a second-party opinion (SPO) for a green or sustainable bond.

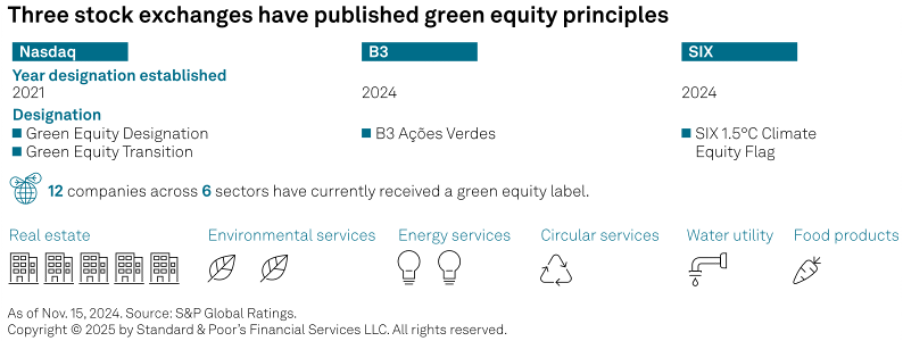

Currently Nasdaq, B3 and SIX offer green-equity designations based on green-equity principles. In addition, the London Stock Exchange offers the Green Economy Mark, based on a data-driven way to identify green companies.

Contributing and building conceptually on the WFE green-equity principles, Nasdaq, B3 and SIX have defined the requirements for a company to be labelled green. Requirements for companies vary across the exchanges, but in many cases include:

- The majority of revenue is green, with restrictions on fossil fuel-based revenue;

- The majority of investments are green;

- Transparency requirements related to taxonomy alignment or other KPIs;

- Annual confirmation that a company still meets the requirements.

While there are only 12 companies that currently qualify across these designations, we see growing interest from both exchanges and companies. The companies that carry a green-equity label are based in a wide range of sectors, from water utilities such as SABESP, to real-estate companies such as Heba Fastighets, and energy services such as Primrock. Several companies have also IPO-ed onto a green designation, for example Solar Foods, a Finnish food-tech company.

As an approved reviewer for Nasdaq, B3 and SIX green equity designations, S&P Global Ratings provides independent assessments of consistency with exchange requirements. We use our Climate Transition Assessment, featuring Shades of Green to look beyond Net Zero targets to understand near term transition actions and investments. In our analysis we apply the Shades of Green approach to a company’s revenues and investments.

Our Shades of Green approach provides transparency on the whole spectrum of transition across the economy, featuring six shades from red fossil-fuel related activities to dark green low carbon climate resilient activities. This spectrum approach allows for different sector and regional starting points in the transition, while also highlighting business activities that are already aligned with a low carbon climate resilient future.

Strong Foundations for Growth

Looking at the underpinnings of the success of the green and sustainable bond market, there are several features that stand out: transparency, flexibility and credibility.

Both green bonds and green equity provide transparent, easily identifiable investments that support a green economy. The first labelled green bond issued by the World Bank in 2008 was in response to demand from investors for a green product. Similarly, the first green equity designation established by Nasdaq provided a way to showcase green companies to investors.

Voluntary principles for both green bonds and green equity provide a flexible yet robust guidance to the market. In 2014, the ICMA built consensus across market actors through the establishment of the Green Bond Principles. These principles have evolved over time, but the strong foundation of transparency remains the basis. In 2024, the WFE published the Green Equity Principles, building consensus across exchanges and providing flexible and transparent guidance for exchanges to draw upon as they establish their own green equity designations. This provides a flexible basis to adapt for regional circumstances and local markets of the exchanges.

Trust has been nurtured through external reviews that provide a third-party opinion on consistency with exchange requirements. From the first labelled green bond, investors asked for an independent review of the green-ness of the use of proceeds. The model for Second Party Opinions was established by the former parent organisation of Shades of Green, CICERO climate-research institute. This independent review model continues to be best practice in the sustainable bond market today. Likewise, approved independent reviewers evaluate a company’s credentials against the requirements of green-equity designations.

Future Prospects for Diversification

Financing the transition to a sustainable future requires all types of financing, from use-of-proceeds green bonds to whole-of-company green equity. To scale up finance for the green transition, this is an opportune time for continued experimentation and evolution.

The pace of transition faces headwinds and tailwinds in different jurisdictions – and with different starting points. The WFE Green Equity Principles provide a strong basis for future refinement and allow for regional variations to reflect local markets. As the pace of transition proceeds according to regional circumstances, the WFE can continue to provide an important forum for exchanges to reflect upon and refine the Green Equity Principles going forward. While the green equity market is nascent, there are promising beginnings for future growth.

Disclaimer:

The views, thoughts and opinions contained in this Focus article belong solely to the author and do not necessarily reflect the WFE’s policy position on the issue, or the WFE’s views or opinions.