Trading Fragmentation and Clearing Consolidation: A Policy Paradox?

Disclaimer: The views expressed in the article are solely those of the author and do not necessarily represent the views of NSE Clearing or NSE.

Introduction

Many markets have multiple exchanges or trading venues for a given product. In such fragmented markets, there are multiple alternatives for organising clearing arrangements. Clearing can be done through multiple captive central counter parties (CCPs) mirroring the fragmentation of trading or alternatively, consolidated clearing can be offered through a common CCP or by implementing CCP interoperability.

Availability of these multiple clearing models raises two key questions – firstly, should the choice of the clearing model be a business/commercial decision of trading venues and CCPs or should it be a matter of public policy? Secondly, does the choice of clearing model affect the trading behaviour under fragmented trading?

I sought to study these questions and shed light on the impact of clearing consolidation on trading behaviour through an original research paper, which was presented at this year’s WFEClear conference. The paper provides a theoretical model for behaviour of informed traders and tests the predictions of the model on empirical data from Indian markets. I find that clearing consolidation leads to more concentration of trading activity of commonly traded products in one dominant exchange. In other words, consolidation of clearing leads to consolidation of trading activity as well. Thus, there is an inherent contradiction in the simultaneous pursuit of encouraging alternative trading venues and clearing consolidation as policy objectives – they are at odds with each other.

Fragmentation of trading and consolidation of clearing

The organisation of exchanges and their linkages with CCPs has traditionally been a business decision. Market participants and infrastructure providers made such decisions based on efficiency, risk management, and commercial incentives. However, in recent years, policymakers seem to view linkages between exchanges and CCPs as a matter of public policy. Notably, in September 2024, Draghi report on European competitiveness recommended consolidation of clearing and settlement systems in EU by creating a single CCP and a single CSD for all securities traded. Taking a different path, the requirements issued in 2018 by Indian regulators mandated the Indian CCPs to put in place interoperability arrangement and clear trades done on all venues.

On the other hand, the regulatory effort in various jurisdictions has been quite the opposite for trading – regulators have sought establishment of additional venues to promote competition among trading platforms. Notably, the Regulation-National Market System (RegNMS) in the USA and the Markets in Financial Instruments Directive (MiFID) in the EU allowed new entrants with different market models as alternative trading venues.

Organisation of trading and clearing arrangements

Exchanges provide a platform for traders with heterogeneous beliefs to come together and discover a price. Due to network externalities and economies of scale, price discovery is more efficient if trading takes place on a single exchange. Exchanges are therefore viewed as natural monopolies. Nevertheless, having multiple exchanges for the same asset has some benefits considering that traders have heterogeneous trading needs and exchanges also have profit motives from administering the marketplace. Multiple trading venues for the same product therefore exist, and compete on several factors such as access requirements, connectivity, colocation services, tick and lot sizes, order transparency, fees and rebate structures etc. Multiple venues also offer some benefits from the policy perspective such as competition, more resiliency to trading outages etc.

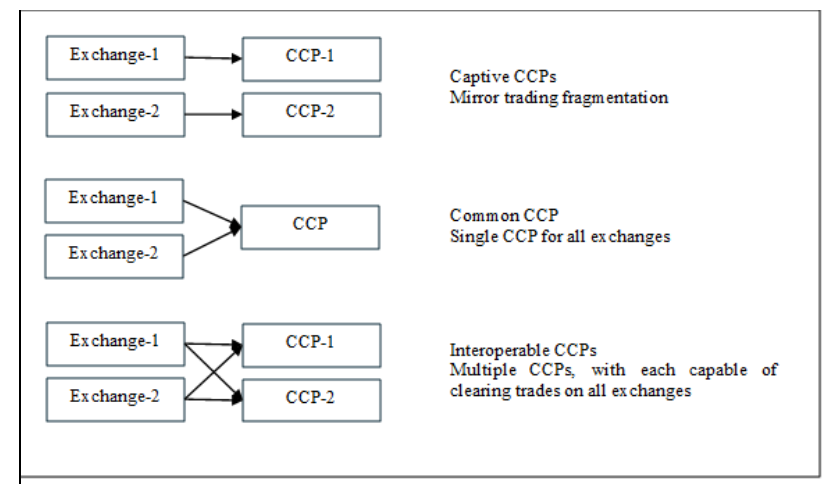

Figure 1: Possible clearing models under fragmented trading

In an environment with multiple trading venues trading in the same security, there are three possible models for organisation of clearing arrangements: (i) most commonly, exchanges operate their own Captive CCPs wherein in trading venue has a dedicated clearing house with one-to-one exchange-CCP linkages. (ii) In some markets, a common CCP clears trades done on multiple exchanges. A prominent example of this model is the US cash equities market where DTCC acts as a single CCP and CSD. (iii) a model of interoperable CCPs is also possible, where trades done on one exchange might get cleared on multiple CCPs. In this scenario, each exchange will be linked with more than one CCPs. This model exists in the EU and India.

Unlike the captive model, a common CCP or multiple interoperable CCPs allow consolidation of clearing for trades done on multiple exchanges. Consolidation of clearing of trades done on multiple exchanges leads to greater netting opportunities, operational efficiency and lower collateral requirements.

Trading fragmentation and impact of clearing consolidation

Current academic literature in the context of dark pools discusses a so-called “Pecking Order Hypothesis”1, according to which informed traders choose venues in order of cost of execution and immediacy, preferring venues with low execution cost and low immediacy first, followed by venues with greater execution cost and greater immediacy. They first prefer midpoint dark pools followed by non-midpoint dark pools followed by lit markets.

I show that the argument can be extended to multiple lit markets. It has been observed over a long time and across asset classes that under trading fragmentation, one venue (“dominant exchange”) often leads the price discovery process, and its discovered price is tracked by other venues (“satellite exchanges”). The spreads are often wider in the satellite exchange but constrained by cost of arbitrage between the two exchanges. The cost of inter-exchange arbitrage is higher when multiple captive CCPs individually clear the trades of multiple exchanges, but the same is substantially reduced if clearing is consolidated through models such as CCP interoperability.

In the research paper, I show that an informed trader having a choice of execution on a dominant and satellite exchange (both lit), prefers improving the best bid/ask on satellite exchange, followed by improving best bid/ask on dominant exchange, followed by crossing the bid-ask spread on dominant exchange. This is similar to the informed trader behaviour predicted by the Pecking Order Hypothesis for dark pools. However, on consolidation of clearing, improving bid/ask on satellite exchange becomes costlier considering narrower spreads for the same likelihood of matching with incoming market orders (better execution price for consuming liquidity means worse execution price for providing liquidity). Thus, the execution preference for the informed trader changes from satellite exchange to dominant exchange as cost of arbitrage is reduced by clearing consolidation.

I tested the predictions of the theoretical model on market data surrounding implementation of interoperability in India. As predicted, clearing consolidation leads to greater preference of informed traders for the dominant exchange (measured using execution of bulk deals in regular order book), leading to reduction in the expected execution price of informed and uninformed traders. As a consequence of the change in the execution strategy of informed traders, the market-wide best buy/sell spreads become narrower, and prices become more informative. These improvements are at the cost of reduction in trading volumes on satellite exchange where liquidity provision is increasingly done by arbitrage traders.

Policy implications

It may appear that the results indicate that market quality is improved on consolidation of clearing – but its not necessarily the case. Consolidation of clearing leads to more concentration of trading in the dominant exchange, more specifically higher execution by informed traders in a common trading venue. Following the Natural Monopoly argument for exchanges, as greater number of traders come together on the same exchange, informativeness of prices increases and adverse selection of uninformed traders reduces. Clearing consolidation lowers fragmentation of trading, and reduced fragmentation of trading improves market quality.

This observation points out a concern about simultaneously pursuing clearing consolidation and promoting trading venue competition as public policy objectives. These will be at odds with each other – consolidation of clearing can trigger consolidation of trading of a given asset in a single venue and having multiple alternative venues for the same product may not be viable.

Disclaimer:

The views, thoughts and opinions contained in this Focus article belong solely to the author and do not necessarily reflect the WFE’s policy position on the issue, or the WFE’s views or opinions.