Amplifying Climate Action and the Power of Nature

Executive Summary: Prioritising Nature and Biodiversity in Sustainability Strategies

In this paper, the World Federation of Exchanges (WFE) addresses a pressing question: Is now the right time to prioritise nature alongside climate issues? Our answer is unequivocal — nature cannot wait. Despite a growing scepticism about sustainability and nature-related issues in some jurisdictions, maintaining momentum on nature is important for the following reasons:

- Amplifying Climate Impact: Nature degradation exacerbates the effects of climate change effects. Ignoring biodiversity risks undermines existing efforts and creates cascading systemic challenges.

- Financial Exposure: Nature-related risks are becoming increasingly financially material, and financial markets are currently failing to price those nature-related risks effectively. This misalignment leaves institutions vulnerable and weakens the global response to environmental crises.

- Frameworks Have Evolved: Advances by the TNFD, ISSB, GRI and CDP have made it feasible to integrate nature into sustainability strategies without disrupting current frameworks and have found a balance to ensure convergence and therefore secured sufficient compatibility to make it decision useful.

For investors to have confidence that they are funding activities that truly are environmentally sound, the businesses must be able to demonstrate their green credentials. This requires disclosure against an objective standard, supporting all market participants in relation to tradable instruments, including derivatives. While standards for carbon emissions are relatively well established, significant progress is now being made in relation to other areas of sustainability, starting with nature.

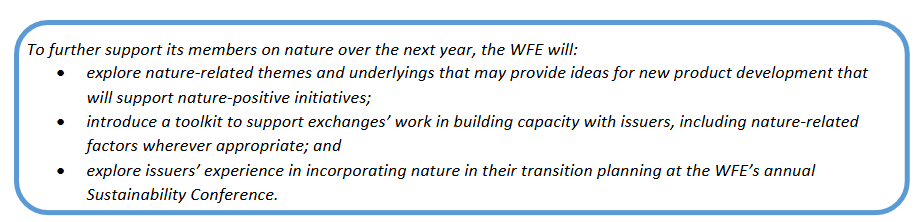

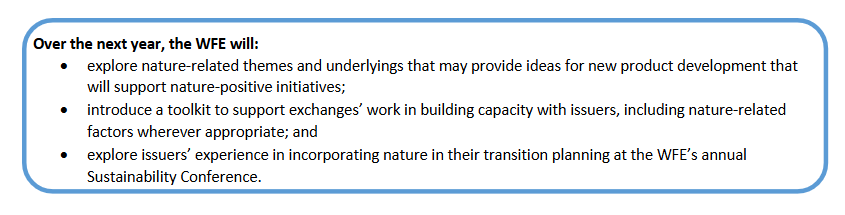

In this paper, we examine the crucial role that public, lit markets will play in tackling nature degradation and the key actions that will enable them to play that role. The paper outlines the actions exchanges are taking to manage their nature-related risks and opportunities and ensure their issuers are doing the same, such as:

Educating and Building Further Capacity: Embed nature reporting in issuer education to refine transition plans, improve Scope 3 emissions data and align with forthcoming EU regulations, which will be of real value in ensuring international investment. | |

Promoting Early Adoption: Facilitate knowledge sharing among issuers to build confidence and capability ahead of regulatory mandates. | |

Identifying Innovative Financial Products: Develop and support biodiversity bonds, equity designations and other nature-related products to channel investments toward conservation efforts. | |

Providing Regional Leadership: Showcase initiatives by exchanges and issuers; share best practices; and enhance global collaboration. |

It is important to note that the priority for many exchanges in their work with issuers and financial service providers, has been to support them with the steady uptake of sustainability reporting globally. Much of these efforts have encouraged international consistency. This global convergence is positive and strongly supported by the WFE and its members as it will enable investors globally to compare information easily and avoids issuers being asked for the same information in different formats. However, it is important to balance this action with the challenges and costs it poses to businesses.

Given the progress in nature reporting, this paper also sets out some recommendations for policymakers and how they can support exchanges’ efforts in this area. It proposes they support these efforts by:

Convening diverse stakeholders to prioritise and fund biodiversity initiatives. | |

Identifying and publishing clear jurisdictional nature risks and priorities, along with recommended actions to guide investment and transition strategies. | |

Considering how nature reporting can be better calibrated globally and considered alongside other requirements to make the balance of reporting more scalable, recognising that the resources of listed companies in some jurisdictions are far more limited than in others (especially as it is often in these same jurisdictions that the dividends of nature reporting will have the greatest impact and will need to attract funding for its protection). | |

Providing continued feedback on progress and changes in national/regional priorities to maintain momentum and showcase good practice that has been particularly effective and partner with exchanges to ensure financial products address critical needs and deliver measurable return on investment. |

The WFE firmly believes that nature is integral to effective global sustainability efforts. By acting decisively now, exchanges can drive transformative change, mitigate systemic risks and lead the financial sector toward a sustainable future. However, we also urge relevant policymakers to think carefully about how to calibrate reporting more effectively to ensure the burdens of expanding the scope of reporting do not make it unmanageable. We also urge national policymakers to identify, in dialogue with national stakeholders, the key priorities to ensure more targeted results, so that reporting leads to clear actionable results for the benefit of all.

Introduction

The dramatic depletion in nature and particularly in biodiversity over recent decades poses significant risks to both the environment and human societies. This paper considers what this means for a different sort of environment – the world of lit, public markets, where issuer disclosures and robust price formation and risk transfer are key.

The Kunming-Montreal Global Biodiversity Framework (GBF) - the nature equivalent of the Paris Agreement for climate change - was adopted in 2022 and set an ambitious pathway toward the global vision of a world living in harmony with nature by 2050, with four goals for that year and 23 targets for 2030. This framework establishes collective commitments for reversing loss of biodiversity and natural habitats, targeting a wide range of stakeholders including governments, corporations, civil society, and investment institutions.

The urgency of action globally to protect and restore biodiversity and natural capital is clear and well accepted, and so focus is turning to how financial institutions price and allocate capital within the economy in order to achieve these goals. The GBF will be an increasingly strong driving force for action, in the same way as the Paris Agreement has been on climate. This itself creates transition risks but also significant opportunities for proactive exchanges. Today, nature risks are not sufficiently priced into financial markets and are not accounted for in the scenarios used by financial institutions, leaving the financial system exposed to potential systemic risks and contributing to the misalignment of objectives. Furthermore, nature will play a crucial role in the fight against climate change.

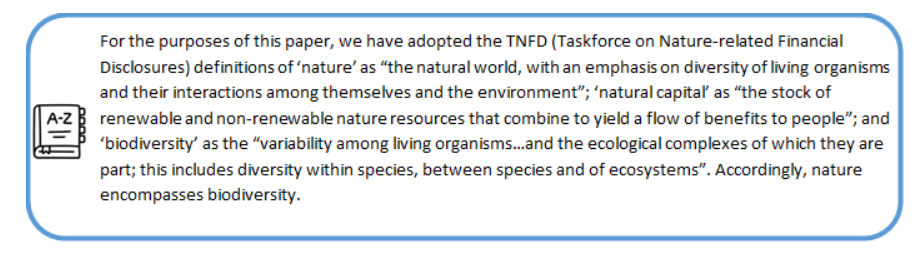

Defining ‘nature’ and the magnificent 7

While there has historically been a lack of standardised nature-related reporting frameworks, this is no longer true. There are seven leading approaches currently used for nature reporting:

- The Carbon Disclosure Project (CDP)

- The European Sustainability Reporting Standards (ESRS)

- The Global Reporting Initiative (GRI)

- The International Sustainability Standards Board (ISSB)

- The Natural Capital Protocol

- The Science Based Targets Network (SBTN)

- The Taskforce on Nature-related Financial Disclosures (TNFD)1 (which will be incorporated into the work of the ISSB going forward).

Each approach has its own distinct features but aims to be interoperable with the others. For example. SBTN is guidance on target setting whereas CDP is a reporting platform that organisations can use to disclose their targets and progress made towards them. Additionally, the definition of materiality varies across approaches, e.g. GRI and ESRS require consideration of both the risks organisations face from nature-related factors and the impacts of organisations’ activities on nature (also known as ‘double materiality’). GRI and SBTN require consideration of environmental and social materiality while the ISSB requires consideration only of the nature-related factors that will affect an organisation’s enterprise value.

The ISSB is attempting to harmonise approaches by incorporating both the GRI and TNFD into its prospective nature-specific reporting standard. Work setting out the interoperability of these standards has already been completed, and the ISSB also released ESRS-ISSB interoperability guidance in June 2024. These various steps reflect that there is a growing international consensus around nature, which will be a key consideration for exchanges and issuers in developing their strategies on nature.

Why is nature important?

| Nature is important for the economy: Half of global economic activity is moderately or highly dependent on natural assets, and more than 55%2 of the world’s GDP is exposed to immediate material nature risk. In the UK alone, damage to the natural environment could potentially lead to a loss in GDP of 12%. To put this in context, this would be larger than the GDP loss caused by both the 2008 Global Financial Crisis and Covid-19 in the UK. On the other hand, nature-based solutions could provide an additional 20 million jobs if, investment is tripled by 2030.3 | |

| Nature has an important role to play in achieving Paris-aligned global goals: For example, land currently stores more carbon than anything else on the planet; unless effort is made to reduce the pace of soil degradation, it is estimated that nearly 70 gigatonnes more carbon could be released into the atmosphere by 2050, due to land use change and soil degradation. This is approximately equivalent to 17% of current annual greenhouse gas emissions.4 | |

Nature reporting is valuable to issuers and investors: More than half of listed companies on the 19 largest stock exchanges are moderately or highly dependent on nature.5 Therefore, nature reporting can provide useful information that is material to investors and is an opportunity to develop strong investor relations. Additionally, nature reporting can provide opportunities for investors and businesses to realise significant financial gains as nature-based solutions could generate up to $4.5 trillion worth of business opportunities by 2030.6 |

COP15 saw global biodiversity targets being set for 2030, including effective conservation and management of at least 30% of the world’s lands, inland waters, coastal areas and oceans.7 The Convention on Biological Diversity has participation from 196 countries.8 As 2030 approaches and governments look to make good on their biodiversity targets, domestic regulators are increasingly introducing new regulations requiring businesses to align with broader nature-related goals and meet the demand for greater public scrutiny of companies’ impacts on nature, which has been increasing from 2014 to 2023.9

Current challenges to effective and timely nature reporting

Businesses may face various challenges in assessing and reporting on their nature-related risks, opportunities and impacts. Below is a list compiled from member feedback gathered by the WFE and desktop research:

| Organisations are still trying to build capacity – and data – on climate factors. They may not currently have sufficient time and resources to dedicate to nature. As with carbon emissions, there needs to be recognition that progress will require a transition over time. There are limited regulatory requirements (and incentives) globally to make companies report on nature, although this is likely to change as international consensus forms around nature-related reporting standards. | |

| The proliferation of nature-related reporting standards, frameworks and regulatory requirements has made it difficult for organisations to navigate what they need to do and what approach they should take. Although progress is being made to introduce standardised reporting frameworks, as outlined earlier in this paper, businesses currently lack clear guidance on nature reporting. | |

| Organisations lack comprehensive and comparable data on nature. Organisations looking to report on their nature-related risks, opportunities and impacts find it difficult to obtain relevant data, particularly from third-party organisations and suppliers. |

In addition to the above, stock exchanges may also need to consider additional safeguards when offering nature-based financial or data products to investors to avoid greenwashing allegations. These safeguards may include nature-related reporting and assurance requirements for issuers.

Businesses can also act now to prepare their operations for new nature-related regulatory requirements aligned with emerging global standards and frameworks. Businesses that take action on nature now will not only stave off the most severe nature-related risks but will also position themselves to take advantage of the opportunities presented by doing so, more detail on which is outlined on the section below.

Opportunities for stock exchanges and issuers related to nature reporting

Nature-related reporting and solutions present various opportunities both for stock exchanges and issuers. Investing in nature-based solutions can not only, help mitigate the adverse impacts of nature deterioration, but can also help reduce climate risk, as well as providing a range of benefits for issuers and exchanges.

Issuers

Enterprise value: Between 2019 and 2022, it was observed that there was a positive correlation between the valuation of a business and its contributions to biodiversity degradation. However, following the UN Biodiversity Conference (COP15), this correlation began to break down. Stocks with large biodiversity degradation footprints began to lose value. This process accelerated following the launch of the TNFD in June 2021.10 It is not unreasonable to expect that this trend will continue as reporting requirements evolve and investors look more rigorously at material nature-related impacts and dependencies.

Collecting and, just as importantly, translating nature-related data to assessments of material risks and opportunities can allow board members to understand the impact of nature dependencies on their business strategy and operations, as well as the impact their business is having on natural resources. Both can be useful in assessing future strategic, operational and financial performance more accurately, arming board members with the information they need to perform their fiduciary duties to shareholders Reporting on nature can also provide an opportunity for issuers to develop strong relationships with investors, who are increasingly looking for information on both business dependencies and impacts on nature.

Net Zero targets: The share of listed companies globally with net zero targets has increased consistently from only 1% in 2017 to 32% in 2023,11 and measures to slow or stop nature deterioration can help companies achieve their net zero goals. For example, oceans are currently the largest natural carbon sinks, absorbing 30% of carbon emissions today,12 while organic soil is the second largest13. Less well known is the incredible role that mangroves play in carbon sequestration and protecting coastal areas in hurricanes14. Mangroves store up to four times more carbon than other tropical forests, making them extremely valuable.15 However, mangroves, like many other critical nature-based solutions, are under threat, with the International Union for Conservation of Nature reporting that more than half of the world’s mangrove ecosystems are at risk of collapse16. It is critical that we secure the future of our natural resources and that financial flows support attempts to do so.17 Exchanges are well placed to support these objectives through the products they develop and the transparency they require from their listed issuers.

Legal and reputational risk management: From an operational and strategic risk level, capturing nature-related information, using it to inform business decisions, and reporting material nature-related dependencies and solutions can reduce both emerging regulatory and reputational risks related to nature. Although nature-specific regulations are not yet widespread, scrutiny by regulators and lawmakers is growing. For example, in Europe the European Sustainability Reporting Standards (ESRS), which require biodiversity transition plans, came into effect in 2024 and the EU Deforestation Regulation (EUDR) will require large companies to demonstrate that their products are deforestation-free from 30th December 2025, followed by SMEs from 30th June 2026. These legislative initiatives create tangible legal and reputational risks for businesses that do not understand and collect data on their supply chains.

Investors

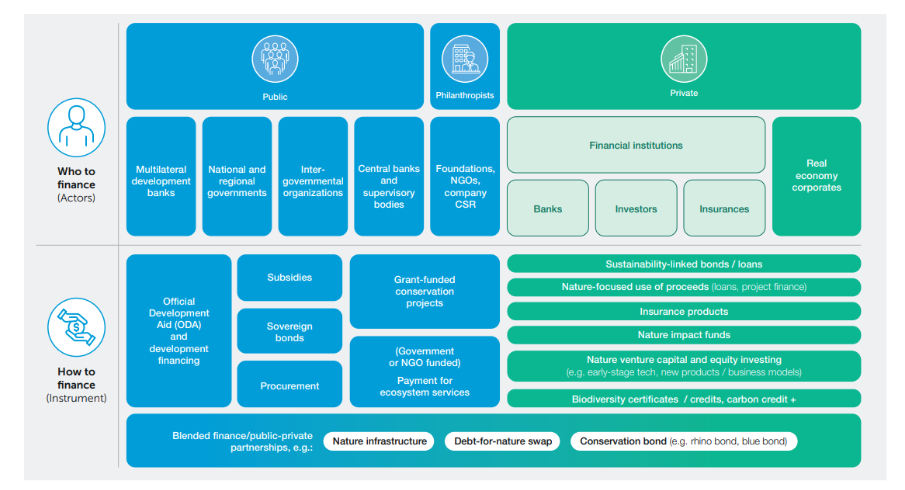

Closing the gap: There is estimated to be a financing gap of over $700bn per year for nature solutions. 18 The financial services industry, centred on market infrastructure (exchanges, together with clearing houses), can help move capital to nature-based solutions, transforming the economy and value chains. This can take place in various ways as outlined below:

Figure 1 - Financing nature - positive transition - examples of who and how to finance (WEF_Financing_Nature-Positive_CEO_Briefing_2024.pdf (weforum.org))

If the private sector were to mobilise around this issue, it is estimated that corporate action could help put natural capital on a path to recovery by 2050.19

Resilient capital flows: Nearly three fifths (58%) of market capitalisation of major Asia-Pacific stock exchanges are in significant nature-related risk sectors. Over half (53%) of Asia-Pacific’s gross value added (i.e. $18tr) is highly or moderately dependent on nature. Stock exchanges themselves are dependent on nature via the composition of their listed companies. For example, at New York Stock Exchange 40% of companies have high or moderate dependence on nature, while 70% of the Taiwan Stock Exchange Corporation’s listed companies have high or moderate dependence on nature.20 More than half of the market capitalisation listed on 19 of the world’s largest stock exchanges is exposed to material nature risks.21

Stock Exchanges

For exchanges, the above apply, but there are additional opportunities related to nature reporting.

Attracting investment: Stock exchanges have a significant role to play in nature-based solutions not only through capital allocation but also because some of the largest enterprises with the most significant impacts on nature are listed on exchanges. For stock exchanges, nature-based solutions and nature reporting can provide a significant business opportunity as high-quality information on nature can attract investors interested in closing the funding gap for nature.

Creating investment opportunities: Stock exchanges provide trusted infrastructure for new and innovative nature-related financial product markets which are likely to see significant growth. Investor demand for nature-related products is growing, with global demand for biodiversity credits estimated to reach $2bn by 2030 and $69bn by 2050.22 Blue bond markets are roughly where green bond markets were 10 years ago and there are now over $10 trillion green bonds in issuance.23 Stock exchanges are taking advantage of this opportunity by developing new products that facilitate investment in nature-positive projects.

Supporting issuers: There is also an opportunity to provide additional value to issuers and investors by providing issuers with relevant guidance on nature reporting. This will support exchanges and their issuers in effectively managing their nature-related risks and opportunities. Additionally, demand for nature-related information by investors can also be met by stock exchanges in various ways, such as through a biodiversity index which will also reward issuers who are proactively incorporating nature into their reporting and transition planning.

What are exchanges doing to support issuers?

There are various ways in which stock exchanges can provide value for and support issuers in their nature reporting journey. These include:

Educational initiatives that explain the value of nature reporting and likely implications of forthcoming regulation, including the extraterritorial impacts of regulations targeting supply chains on issuers that will be affected. | |

Encouraging nature reporting by sharing good practice before regulatory reporting requirements are imposed so that issuers can prepare their business and build capabilities on nature. Sharing case studies and experience can highlight how early adopters have identified and addressed key challenges with due regard to international standards. | |

Creating and facilitating the trading of nature-based product offerings such as biodiversity bonds and enabling issuers to market their sustainability credentials, e.g. through green and sustainability-related equity designations (including equity labels and flags. |

How can policymakers support exchanges’ efforts in this area?

Convene diverse stakeholders to prioritise and establish what is needed to fund biodiversity initiatives. Convene stakeholders, including but not limited to indigenous peoples, farmers and industries active in their region, to establish consensus on the biggest risks and to identify what needs funding (so that exchanges and others can begin to think about products that could support these initiatives). This will ensure transition plans and projects are more effectively targeted and results are more visible and tangible. | |

Identify and publish clear jurisdictional nature risks and priorities, along with recommended actions to guide investment and transition strategies. Having established consensus on jurisdictional nature risks and priorities, publish this information and any proposed actions so that international investors, local industry, companies being supplied by the local industry, exchanges and financial service providers can more effectively align investments and transition plans with these elements. This will support exchanges in developing their sustainability offerings and turning data into tangible action. | |

Advance international consistency and carefully balance requirements with burdens Recognising that the resources of listed companies in some jurisdictions are very limited and reporting is costly, it will be critical to consider the impact that requirements will have on companies, particularly SMEs. In a global context, it is also important to bear in mind that ‘traditional’ definitions of a SME may not be appropriate for all markets as absolute measures developed for European companies may not reflect the relative position of businesses in other markets. Effective calibration to jurisdictional realities is critical to a just transition. This is particularly true in relation to nature, where issuers in jurisdictions with some of the most natural capital have the most limited resources. It is important that the policy landscape enables these regions to realise the dividends of their natural resources and secure funding for their protection. To achieve this, policymakers must think carefully about the balance of incentives and broader implications of their policies on these very fragile but critical markets and issuers where margins are often limited. | |

Provide continued feedback and communication on priorities. Provide continued feedback on progress and changes in national/regional priorities to maintain momentum and showcase good practice that has been particularly effective. Identify and promote issuers internationally that have successfully integrated nature into their reporting and turned that reporting into action. | |

Partner with exchanges to ensure financial products address critical needs and deliver measurable returns on investment. Consider how partnerships with exchanges and financial service providers could ensure financial products are channelling financial support to where it is most needed and work with exchanges to demonstrate the return on investment achieved. |

Conclusion

While the exact path forward may not be entirely mapped out yet, it is nonetheless clear that - as with carbon emissions - the interaction between the financial world and the natural habitat is going to come increasingly into focus. In the short term, this will require an emphasis on international consistency to avoid arbitrage and ensure that a concerted effort is made to support efforts to address nature degradation.

Given that nationally determined targets will be reviewed by 2030 and that by this point international consensus on nature reporting frameworks will have progressed, the pace of regulation will likely not be far behind.

Given the pace of regulation, implementing each development consecutively will not be an efficient, or even effective, way to design an organisational approach to nature and sustainability issues more broadly.

Instead, businesses should plan to adopt a holistic approach to their sustainability strategy that is flexible enough to accommodate domestic regulation, international best practice and evolving investor expectations.

As the constant demand and expansion of sustainability regulation continues, we urge policymakers to be increasingly mindful that more creative and effective ways to scale reporting need to be developed. Regulatory requirements should be considered in their broader sustainability and economic context and calibrated with global differences in mind. A careful balance must also be struck between the cost for businesses and the need for practical action if climate change and nature depletion are going to be addressed effectively. To strike this balance, policymakers must ensure that jurisdictional realities such as differing developmental and environmental priorities that impact policymaker resources, are factored into efforts to develop and promote international baselines and consistency in this space.

In conclusion, when one considers that the words ‘economy’ and ’ecology’ come from the same epistemological root — ‘economy’ literally meaning managing one’s environment and ‘ecology’ meaning understanding the environment — it may not seem such a strange challenge. The current system may not sufficiently link the two, but it is possible to close the gap and doing so will be critical if we want to avoid the most damaging impacts of climate change.

Background

Established in 1961, the WFE is the global industry association for exchanges and clearing houses. Headquartered in London, it represents over 250 market infrastructure providers, including standalone CCPs that are not part of exchange groups. Of our members, 37% are in Asia-Pacific, 44% in EMEA and 19% in the Americas. WFE’s 87 member CCPs and clearing services collectively ensure that risk takers post some $1.3 trillion (equivalent) of resources to back their positions, in the form of initial margin and default fund requirements. WFE exchanges, together with other exchanges feeding into our database, are home to over 51,000 listed companies, and the market capitalisation of these entities is over $110 trillion; around $140 trillion (EOB) in trading annually passes through WFE members (at end 2024).

The WFE is the definitive source for exchange-traded statistics and publishes over 350 market data indicators. Its free statistics database stretches back more than 40 years and provides information and insight into developments on global exchanges. The WFE works with standard-setters, policymakers, regulators and government organisations around the world to support and promote the development of fair, transparent, stable and efficient markets. The WFE shares regulatory authorities’ goals of ensuring the safety and soundness of the global financial system.

With extensive experience of developing and enforcing high standards of conduct, the WFE and its members support an orderly, secure, fair and transparent environment for investors; for companies that raise capital; and for all who deal with financial risk. We seek outcomes that maximise the common good, consumer confidence and economic growth. And we engage with policymakers and regulators in an open, collaborative way, reflecting the central, public role that exchanges and CCPs play in a globally integrated financial system.

If you have any further questions, or wish to follow-up on our contribution, the WFE remains at your disposal. Please contact:

Victoria Powell, Senior Manager Regulatory Affairs: [email protected]

Rona Nairn, Regulatory Affairs Manager: [email protected]

Richard Metcalfe, Head of Regulatory Affairs: [email protected]

or

Nandini Sukumar, Chief Executive Officer: [email protected].

1 https://www.unepfi.org/wordpress/wp-content/uploads/2024/01/Accountability-for-Nature.pdf

2 https://www.mckinsey.com/capabilities/sustainability/our-insights/where-the-worlds-largest-companies-stand-on-nature#/

3 Nature-based Solutions can generate 20 million new jobs, but “just transition” policies needed (unep.org)

4 Land - the planet’s carbon sink | United Nations

5 sbpwc-2023-04-19-Managing-nature-risks-v2.pdf

6 https://www.pwc.com/gx/en/issues/esg/nature-and-biodiversity/closing-the-nature-investment-gap.html

7 COP15: Global biodiversity framework - House of Lords Library (parliament.uk)

8 COP15: Final text of Kunming-Montreal Global Biodiversity Framework | Convention on Biological Diversity (cbd.int)

9 2m99ku4fsw_Road_to_COP30_briefing_pack_FINAL_.pdf (worldwildlife.org)

10 *Do investors care about biodiversity? (silverchair.com)

11 https://www.statista.com/statistics/1319975/share-of-net-zero-targets-issued-by-publicly-listed-companies-worldwide/

12 Oceans absorb 30% of our emissions, driven by a huge carbon pump. Tiny marine animals are key to working out its climate impacts - CSIRO

13 Soil, land and climate change — European Environment Agency (europa.eu)

14 https://www.worldwildlife.org/stories/mangroves-as-a-solution-to-climate-change

15 Mangroves as a solution to the climate crisis | Stories | WWF (worldwildlife.org)

16 https://iucn.org/story/202405/first-ever-global-assessment-iucn-red-list-ecosystems-reveals-more-half-worlds

17 Mangroves as a solution to the climate crisis | Stories | WWF (worldwildlife.org)

18 https://www.weforum.org/agenda/2024/01/how-biodiversity-credits-can-finance-nature-positive-outcomes/

19 Nature in the balance: What companies can do to restore natural capital | McKinsey standards.

20 AIGCC-PwC-Nature-at-A-Tipping-Point_14-5-24.pdf

21 sbpwc-2023-04-19-Managing-nature-risks-v2.pdf

22 Knowledge Hub | Biodiversity Credits (weforum.org)

23 Blue bonds: Accelerating Sustainable Ocean Business | UN Global Compact