Global delisting trends

Written by Dr Ying Liu, Financial Economist at the WFE

Stock delisting refers to the removal of a company’s stocks from trading on a stock exchange. Delistings generally fall into three broad categories depending on the reason for delisting: 1) involuntary delisting, resulting from bankruptcy, liquidation, or failure to meet listing requirements of exchanges; 2) voluntary delisting, often associated with firms going private, or withdrawing from exchange-based trading; 3) Merge and Acquisition (M&A), where listed companies are acquired or absorbed by other firms.

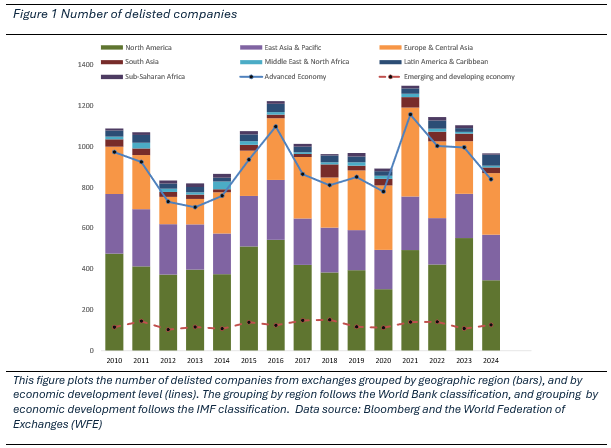

In contrast to initial public offerings (IPOs) which represent new companies being listed, delistings represent the exit of listed companies from the public markets. Understanding delisting trends is as important as understanding the trends in IPOs. Figure 1 plots the number of delisted companies from exchanges grouped by region and by economic development from 2010 to 2024. The sample covers 69 global exchanges from 64 jurisdictions. The global trend exhibits clear cycles of contraction and expansion. Two pronounced spikes appear around 2016 and 2021. The 2016 increase coincides with a wave of voluntary delistings, often motivated by valuation gaps and evolving regulatory expectations (Figure 2). The 2021 spike aligns with the post-pandemic rebound in corporate activity, particularly M&A that generated a large number of delistings, as listed companies were acquired or taken private.

North America consistently contributes a substantial share of global delistings, largely reflecting its large base of listed companies. East Asia & Pacific shows a steadier trend with moderate fluctuations, while Europe & Central Asia exhibits a pattern similar to North America, though with smaller magnitudes. Advanced economies tend to experience a much higher volume of delistings, whereas emerging and developing economies (EMDEs) exhibit a more stable trend. This contrasts with IPO activity, where EMDEs show fluctuations similar to those in advanced economies (World Federation of Exchanges, 2025). The divergence in delisting patterns likely reflects both the ongoing expansion of EMDE exchanges and the gradual increase in firm turnover as these markets continue to mature.

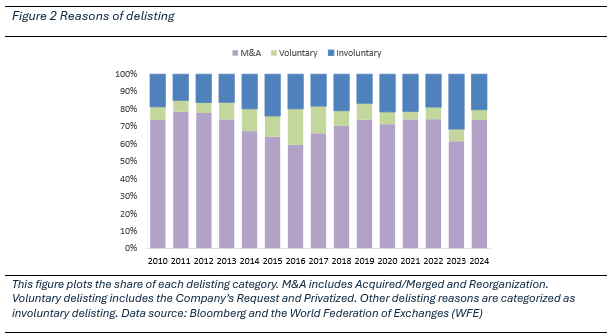

Firms delist for different reasons. Figure 2 illustrates the composition of delisting reasons over time. Among the three reasons, M&A constitutes a significant portion of total delisting, which counts for more than 60% of the total delistings. Voluntary counts for a small portion of the total delisting, generally below 10% of each year. However, 2016 observes a notable spike of go private transactions. Lastly, the number of involuntary delisting remains small but exhibits clear cyclical sensitivity: their share rises in periods of economic stress, such as in 2023, when around 30% of delistings were involuntary. The increase in 2023 is consistent with a more challenging macro-financial environment. After a prolonged period of ultra-low interest rates and policy support during the early stages of the covid pandemic, firms in 2022–2023 faced higher funding costs, tighter credit conditions, and weaker equity valuations. For financially weaker issuers, this combination can lead to persistent non-compliance with listing requirements, trading suspensions, or bankruptcy, all of which ultimately appear as involuntary delistings.

Taken together, the composition and timing of delistings provides insight on economic stability and corporate lifecycle dynamics. Markets with a high share of voluntary and M&A delistings generally reflect strategic corporate restructuring, whereas a large share of involuntary delistings may indicate heightened market stress or weaker firm fundamentals.

References

World Federation of Exchanges. (2025, January). Global IPO Trends. Retrieved from WFE Focus: https://focus.world-exchanges.org/statistics/articles/global-ipo-trends