How Trade Credit Could Deepen Settlement Liquidity

Clearing has made markets safer. Settlement liquidity has not kept pace. Each central counterparty (CCP) nets efficiently inside its own rule book and netting set, but across CCPs, intermediaries, settlement assets and real-economy receivables, obligations sit in separate silos. Further opportunities for netting are thus restricted, forcing institutions to hold fragmented liquidity, making things harder to manage exactly when markets are under pressure.

In our WFE Clear 2026 paper we set out a complementary settlement layer that finds safe offset paths across verified obligations from more than one clearing silo. Our argument here is that this is the next step worth taking.

Key takeaways

- Multilateral setoff can reduce gross settlement cash needs by extinguishing closed chains of obligations across CCPs and their members, without novation and without loss mutualisation.

- Trade credit is a large and stable source of real-economy liquidity, but most of it sits outside formal settlement infrastructure. Multilateral setoff can unlock this source of liquidity

- The practical challenge is governance: verified obligations, legal finality, privacy controls, and clear interoperability with existing CCP processes.

Why CCP netting still leaves value on the table

CCPs are good at the problem they were built to solve. They novate trades into a hub-and-spoke structure, calibrate margin to risk and concentrate default management in a single place.

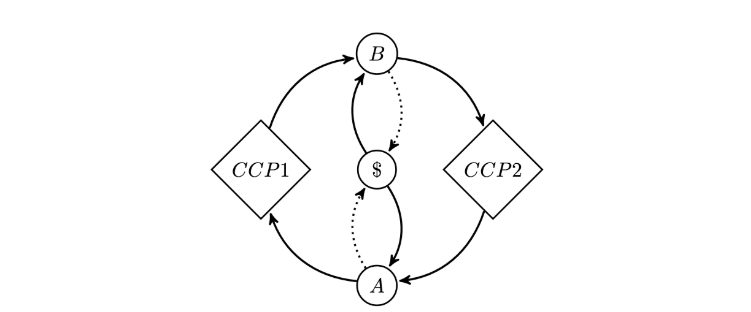

But CCPs only net inside their own netting sets, and there are many CCPs. When obligations alternate across CCPs, some offsetting paths survive silo-by-silo clearing untouched. In a small stylised network with two non-interoperable CCPs, a closed cycle can run A → CCP1 → B → CCP2 → A; each CCP nets its own legs correctly, and yet the cycle of payment obligations remains. The cycle that could be cleared has to be funded with additional money depicted as a central node in the graph (Figure 1).

Figure 1. A small stylised network with two non-interoperable CCPs (CCP1, CCP2) and two traders (A, B). The cycle A → CCP1 → B → CCP2 → A would cancel on a single integrated graph; under fragmented clearing it has to be funded through the central cash node ($).

Multilateral setoff on an integrated graph discharges the cycle and leaves only residual imbalances to fund. This is balance-sheet compression: the same obligations that look unmatched silo-by-silo can form a closed cycle once both silos are visible at once. While novation reallocates and manages counterparty risk, setoff extinguishes matching obligations. Confusing the two leads to suboptimal design choices and capital inefficiency. Incorporating multi-lateral setoff into the network of CCPs and their members reduces the gross volume of obligations to be settled.

The stylised network above is still only focused on financial institutions. We can connect it into the real economy by incorporating trade credit into the graph.

The hidden liquidity outside post-trade infrastructure

Trade credit is everywhere in the real economy. Suppliers extend credit to customers. Buyers carry payables. The aggregate is large: across advanced economies, accounts payable on the balance sheets of non-financial firms are roughly three times the size of bank loans and 15 times the size of commercial paper, and trade credit balances run at around 20 percent of GDP, a ratio that has been stable for 25 years.

The obligations have real economic value. The barrier to using them in settlement is structural: trade credit is bilateral, weakly standardised, and not settlement-ready.

Trade credit has lived in the working-capital conversation. Post-trade has worked with cash and securities.

This is where market infrastructure has something to offer. Exchanges, CCPs and central securities depositories (CSDs) know how to make obligations standard, verified, legally final and operable at scale. Apply those principles to verified trade credit and a sizeable share of these obligations becomes usable for settlement, with the right rules around it.

From cash-only settlement to verified obligation graphs

The core idea is to represent obligations as edges in a directed graph of interlocking balance sheets. Alongside obligations, the Cycles Protocol also introduces acceptances: pre-authorised commitments to receive a given form of settlement, represented as a different kind of edge in the same graph. A closed loop of obligations and acceptances can settle atomically when each leg is valid and pre-agreed.

Acceptances are new.

An obligation is a debt already owed. An acceptance is a pre-authorised commitment to an obligation in the future; when the cycle that contains an obligation is executed, the acceptance becomes an enforceable obligation in the other direction. Once you incorporate acceptances, every settlement can be represented as a cycle.

Together, obligations and acceptances put past debts and forward commitments onto the same graph. Most of finance concerns the future, so settlement cycles can be discovered and executed across the past and future at once.

The resulting protocol is a neutral settlement layer. It runs multilateral setoff on the graph itself, without becoming a counterparty, novating trades, or taking on either side's credit risk. The bridge to trade credit runs through banks and broker-dealers that clear at CCPs and also hold commercial relationships, carrying trade-credit receivables and payables alongside their CCP-facing positions.

Once trade credit enters the graph in verified form, receivables and payables sit on the same graph as variational margin flows, final delivery and the rest of the legs that already run through intermediaries. They become offset paths in their own right. Tokenised commercial bank money, stablecoins or central bank money can sit underneath as the settlement medium. Different settlement assets can appear within one cycle, denominated in a single unit of account.

What must be true for this to work

Three conditions matter. They are operational rather than conceptual.

Double ascertainment. Every receivable or payable entering the clearing graph must be confirmed by both debtor and creditor. Disputed, unverified or stale obligations stay out. The point is to push verification work upstream of settlement, into the contract layer, rather than into dispute resolution after the fact.

Legal finality. A cover contract or rulebook pre-authorises multilateral setoff and defines finality. Without legal finality, setoff is a software operation without settlement effect. For trade credit, this can rest on general obligation law, which is less complicated and less restrictive than payment-system regulation and applies in any jurisdiction where setoff is recognised. Existing trade-credit clearing arrangements in Slovenia, Spain, Italy and Australia already operate on this basis.

Operational and privacy controls. Participants need auditability, confidentiality and well-defined failure handling. Privacy-preserving verification should not require public disclosure of commercial relationships, which is why zero-knowledge cryptography and trusted execution environments are part of our protocol design.

None of these is unsolved.

Evidence and next step

The main evidence we have to-date comes from Slovenia, where multilateral trade-credit clearing has operated in its current form since 1991. The empirical work in our 2020 paper and in the WFEClear 2026 paper points to a finding we keep coming back to: specialised firms emerged inside the clearing network and made it work. They bought receivables, took on credit risk that the network could not absorb on its own, and funded participants at the bottlenecks where cycles would otherwise stall. By the same logic, in a market-infrastructure setting, that role would fall to banks, broker-dealers and specialised funding firms that sit at the interface between CCP clearing and trade credit, operating inside the post-trade obligation graph.

The pilot we would like to pursue is a controlled run with a market infrastructure, its clearing members and selected real-economy counterparties, on a curated set of verified obligations over a defined window. It would measure gross settlement cash reduction, legal enforceability, operational reliability and behaviour under stress. A parallel design conversation under WFE auspices on eligibility rules, the cover-contract architecture and cross-jurisdictional finality would help shape rules that fit alongside existing CCP processes.

Conclusion

The discipline that markets already apply to securities and derivatives can stretch further. Multilateral setoff can bridge liquidity bottlenecks across CCP silos, deepening liquidity and broadening access without incurring additional novation or default management overhead. Trade credit already finances production and trade; it can also become part of how settlement works. For exchanges, this matters because settlement liquidity shapes market access, resilience and the connection between listed markets and real-economy financing. Done carefully, verified trade-credit settlement complements existing CCP risk management. It cuts avoidable gross liquidity needs and starts to bridge public markets with the real economy. The path to trade-credit inclusion is long. Our early work has been in crypto payments and crypto OTC settings. What we need as a next step is to put it in front of real rulebooks.

For more information, please get in touch with the authors at Cycles Protocol: Tomaž Fleischman, Principal Scientist & Co-Founder – tomaz@cycles.money – and Ethan Buchman, CEO & Co-Founder – ethan@cycles.money. Or visit cycles.money.