Stock Exchanges at Scale: Trends, Trade-offs and Implications

Written by Dr Erfan Ghofrani

In recent decades, stock exchanges—the beating hearts of global capital markets—have been quietly undergoing a transformation, in the form of consolidation, integration, and cross-border partnerships. Mergers and platform-sharing initiatives are reshaping the competitive landscape, concentrating trading activity in fewer hands. This raises a critical question: as exchanges grow, what are the implications not just for market concentration and competition, but for market quality and the performance of the exchanges themselves?

At their core, stock exchanges are platforms where companies raise capital and investors trade assets. Historically, exchanges—from the major hubs in developed markets to emerging ones in Asia, Africa, and the Middle East—have evolved to serve local financial ecosystems. However, globalization, technological integration, regulatory changes, and the pursuit of efficiency have ushered in a new dynamic—fuelling consolidation, partnerships, and deeper integration.

Proponents of consolidation, integration and partnerships argue that integrated markets enhance liquidity, lower costs, and improve access to capital. For instance, the 2024 Draghi Report on EU competitiveness contends that fragmented capital markets as a barrier to growth and champions deeper integration through the proposed Capital Markets Union (CMU). For more information, please see here.

Consolidation, integration, and partnerships among stock exchanges can increase market concentration by aggregating trading activity, market capitalization, and listings onto fewer platforms. This aggregation often results from network effects and economies of scale, which make combined platforms more attractive to issuers and investors. Consequently, a smaller number of exchanges control a larger share of global market activity. Critics warn that this growing concentration may reduce competition, raise costs for issuers, and create barriers to entry for smaller or emerging exchanges. As an example, please see here.

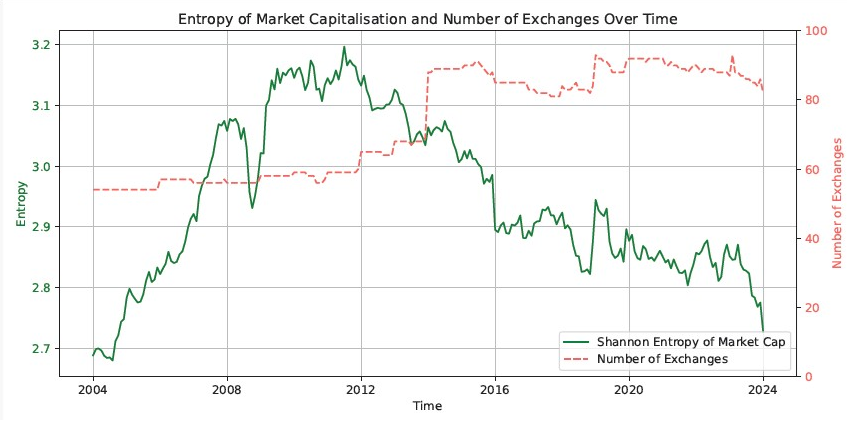

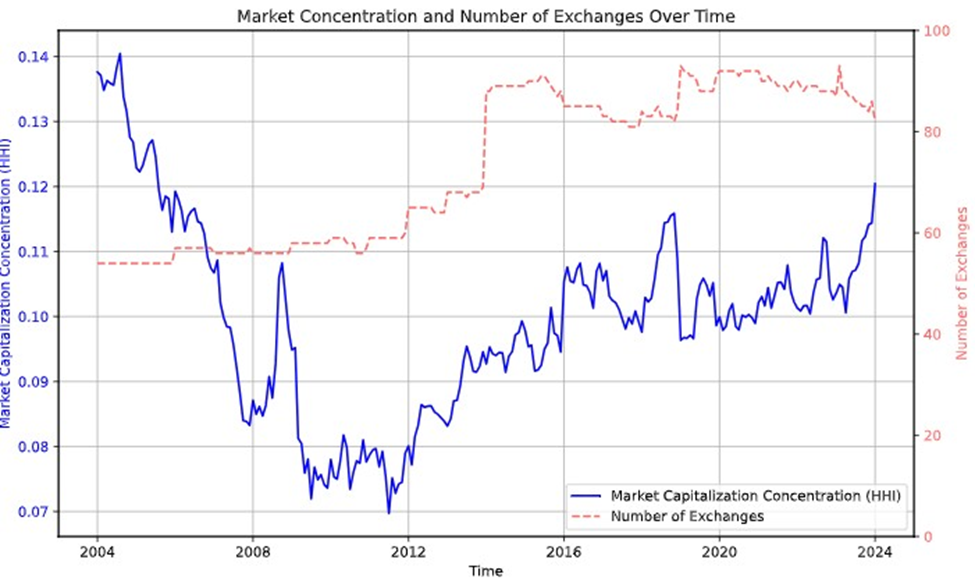

Using data, can we empirically observe an increase in market concentration among stock exchanges? Figures 1 and 2, based on data from the WFE statistics portal, illustrate the evolution of market capitalization concentration measured by two standard measures of market concentration: the Herfindahl–Hirschman Index (HHI) and Shannon entropy. Both figures also show the number of exchanges covered by the WFE Statistics Portal from 2004 to 2024. Although the application of these measures of market concentration has some limitations (e.g., they do not consider barriers to entry, network effects, or the case of double listings), they still can offer some valuable insights.

A higher HHI indicates greater market concentration and potentially reduced competition, while a lower HHI reflects a more competitive market. Figure 1 shows that the HHI fluctuates along a long-term trend, with distinct patterns before and after 2012. From 2004 to 2012, the HHI declined, signalling a reduction in concentration—likely driven by increased competition among exchanges, more evenly distributed market capitalization, a rise in the number of exchanges globally, or broader data coverage by the WFE database.

After 2012, however, the HHI exhibits a sustained increase, indicating rising market concentration. Notably, this period also saw an expansion in the number of exchanges covered by the WFE. This suggests that the increase in HHI is driven by the growing market share of certain exchanges and not by a decline in the overall number of exchanges. It is worth noting that the HHI remains between 0.07 and 0.12 during this period, suggesting the market remains relatively competitive despite the upward trend. Please note that HHI presented in the graph is in decimal form.

Shannon entropy, on the other hand, captures diversity in market share distribution: higher entropy signals lower concentration and greater competition, while lower entropy indicates the opposite. Figure 2 shows a similar trend to Figure 1, highlighting a recent increase in market concentration.

Several factors may explain this trend in market capitalization concentration. A potential driver is the consolidation of exchanges through mergers and acquisitions, which increases the market share of the combined entities. Another factor could be heightened supply-side pressure, with issuers increasingly choosing to list on a select group of exchanges—often due to stronger reputations, higher liquidity, or the appeal of cross-border capital flows. On the demand side, growing investor interest in securities listed on these exchanges may raise their market capitalization and further boost their market share. Together, these dynamics could help account for the recent rise in concentration.

Figure 1 – Market Concentration among Exchanges (HHI)

Figure 2 – Market Concentration among Exchanges (Shannon Entropy)