Tracking Progress in Carbon Offset Futures

Written by Dr Ying Liu, Financial Economist at the WFE

A significant milestone in the evolution of voluntary carbon markets (VCMs) has been the introduction of carbon offset futures, which could enhance liquidity, price transparency, and market scalability. The Global Emissions Offset (GEO) Futures contract was launched in March 2021 as an exchange-traded instrument in the voluntary carbon market. It was later joined by the Nature-Based Global Emissions Offset (N-GEO) Futures in August 2021 and the Core Global Emissions Offset (C-GEO) Futures in March 2022. These standardised contracts allow market participants to trade voluntary carbon credits with greater confidence in their quality and credibility.[1]

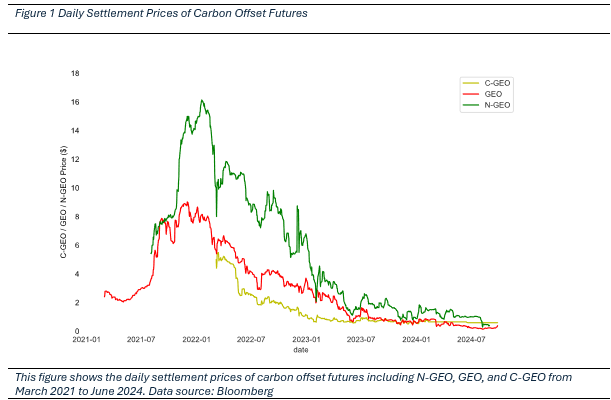

Among the three products, N-GEO consistently trades at the highest prices, followed by GEO and C-GEO. The premium on N-GEO likely reflects its exclusive focus on Agriculture, Forestry, and Other Land Use (AFOLU) projects, which are widely regarded as high-quality offsets. These projects often generate co-benefits such as biodiversity preservation and support for local communities, contributing to stronger buyer preference. In contrast, GEO and C-GEO may be priced lower due to differences in buyer demand.

To assess market liquidity, we examined weekly data and calculated several liquidity and risk measures. The results are summarized in Table 1 and reveal significant heterogeneity among the three offset futures.

Table 1 Summary Statistics of Carbon Offset Futures | ||||||||||||||||||||||||||||||||||||

| ||||||||||||||||||||||||||||||||||||

This table presents summary statistics for carbon offset futures (C-GEO, GEO, and N-GEO) using weekly data from March 2021 to June 2024. Price refers to the weekly closing price in USD. Return represents the weekly percentage return, adjusted for the risk-free interest rate. Volume is the total number of contracts traded per week. Quoted Spread measures market liquidity, calculated as the mean of daily quoted spread of a week. Daily quoted spread is the percentage difference between bid and ask prices divided by the mid-price. Amihud is the mean value of daily amihud ratio, and the daily amihud is calculated as the absolute return divided by the cash volume of a day. Zero Days denotes the average number of days with no trading activity of a week. Volatility is the standard deviation of weekly returns. |

N-GEO stands out as the most liquid product. It has the highest weekly trading volume at 1,102 contracts and the tightest quoted spread at 10.51 percent. The low Amihud ratio of 0.35 suggests low price responsiveness to trading volume which is an indication of high liquidity. Additionally, it exhibits near-continuous trading activity, with virtually no zero-trading days per week.

GEO follows, with a volume of 781 contracts per week and a moderately tight spread of 14.29 percent. It has a slightly higher Amihud ratio than N-GEO, and experiences fewer than one zero-trading day per week, indicating growing but not yet fully established liquidity.

C-GEO currently shows the weakest liquidity indicators. It has the lowest average trading volume (304 contracts), the widest quoted spread (26.64 percent), and the highest Amihud ratio (5.91). It also records the most zero-trading days, averaging over two per week, which reflects its more limited engagement among market participants.

All three products exhibit relatively high return volatility (10-14%), highlighting the evolving and dynamic nature of voluntary carbon offset markets.

Derivatives play a central role in the development of carbon markets. They enable companies to hedge exposure, meet climate-related obligations, and manage risk more efficiently. Just as importantly, they contribute to price discovery and market transparency, which are essential features of a credible and efficient carbon trading system. The emergence of voluntary carbon offset futures reflects growing interest in these tools.

Voluntary carbon markets are inherently diverse, with a wide range of project types, credit standards, and verification systems. This structural variety contributes to differences in perceived credit quality and investor demand. At the same time, it allows market participants to tailor offset strategies to specific environmental and strategic goals. The variation in market performance across N-GEO, GEO, and C-GEO futures reflects this underlying diversity. As infrastructure and market understanding continue to improve, and with ongoing support from exchanges and institutional players, voluntary carbon futures are well-positioned to grow in liquidity, enhance credibility, and play a meaningful role in global climate finance.

Figure 1 presents the daily settlement prices of carbon offset futures. From 2021 to early 2022, offset futures experienced a steady upward trend, with prices peaking at around $15. This reflected growing demand driven by rising corporate climate commitments and increasingly stringent regulatory expectations. However, the outbreak of the Russia-Ukraine conflict in early 2022 triggered a sharp decline in prices due to geopolitical uncertainty and disruptions in global energy markets. Another wave of price volatility occurred in September 2022 during the global energy crisis, leading to a continued downward trend in futures prices. Additionally, in 2023, market sentiment was affected by a series of critical reports on the voluntary carbon market suggesting that certain rainforest-related carbon credits may have been overstated in terms of their climate impact.[2] As a result, prices continued to decline.

[1] GEO Futures facilitate the delivery of CORSIA-eligible carbon credits from registries such as Verra, the American Carbon Registry (ACR), and the Climate Action Reserve (CAR). N-GEO Futures focus on nature-based offset projects listed in the Verra registry, particularly those under the Agriculture, Forestry, and Land Use (AFOLU) category. C-GEO Futures provide a standardised contract aligned with Core Carbon Principles, supporting high-quality voluntary offsets.

[2] See for example: https://www.theguardian.com/environment/2023/jan/18/revealed-forest-carbon-offsets-biggest-provider-worthless-verra-aoe